1. Executive Summary

Alibaba Group is a leading global digital economy company, with businesses spanning China and international commerce, cloud computing, local services, logistics, and digital media & entertainment. After navigating a period of challenges, the company's FY2025 Q3 results show a steady recovery, with total revenue reaching RMB 280.15 bn, up 7.6% YoY – a clear acceleration from the previous quarter – mainly driven by a gradual rebound in its core e-commerce business and a renewed acceleration in the cloud computing segment fueled by AI.

Looking ahead, although the core e-commerce segment faces traffic and competition pressures, its stable cash flows continue to provide strong support for the Group's other businesses. The cloud computing business is entering a new expansion cycle, and large-scale investments in AI infrastructure are expected to deliver substantial growth momentum in the coming years.

On valuation, we employ a sum-of-the-parts (SOTP) approach, assigning a 9× EV/EBITA multiple to the core e-commerce business and a 3× EV/Revenue multiple to the cloud computing business. Our overall valuation is relatively conservative, reflecting each segment's future potential and the uncertainties they face.

2. Company Business Overview

Alibaba Group is a leading digital economy company in China and globally, with operations spanning multiple areas, including:

China Commerce

- Core e-commerce business: Includes platforms such as Taobao and Tmall, which constitute Alibaba's primary revenue source.

- New retail direct operations: Exemplified by Freshippo, which drives the development of new retail formats through an online-offline integrated model.

- Wholesale: Primarily conducted via the 1688 platform for B2B transactions.

International Commerce

- International retail and wholesale: Covers markets in Southeast Asia (Lazada), the Middle East (Trendyol), and Europe (AliExpress), serving overseas consumers and small-to-medium enterprises (SMEs), and currently exhibiting rapid expansion.

Local Services

- Service platforms: Includes Ele.me, Amap, and other platforms, covering food delivery, transportation, and local lifestyle services. This segment is currently loss-making, but its losses have been gradually narrowing.

Logistics (Cainiao Network)

- Logistics solutions: Provides cross-border and domestic logistics services. Profitability had improved previously, but recent internal business adjustments and rising cross-border fulfillment costs have led to margin volatility.

Cloud Intelligence (Alibaba Cloud)

- Cloud services platform: The leading cloud platform in the Asia-Pacific region, offering fundamental cloud services, AI computing power, and big data application support, and continuously driving upgrades in product mix and profitability improvements.

Digital Media & Entertainment

- Content platforms: Includes Youku, Alibaba Pictures, and other content platforms, primarily focused on online video and content distribution services.

Other Innovative Businesses

- Strategic new initiatives: Encompasses DingTalk, AliOS, and other strategic new businesses, which are in a phase of heavy investment and rapid R&D.

3. Value Driving Factors

1. Core E-commerce

Revenue Drivers:

- Platform commissions & transaction fees: GMV scale and higher commission rates are the most fundamental revenue sources.

- Online marketing (advertising): Keyword search and display ads placed by merchants, contributing high-margin revenue.

- Value-added services & memberships: B2B platform membership fees, cross-border logistics services, and paid programs like the 88VIP membership.

- Self-operated retail: Encompasses a small number of self-operated categories (e.g. supermarket and fresh goods), which add revenue but at relatively lower margins.

Cost Drivers:

- Technology & platform operations: Large-scale IT infrastructure investments, as well as product R&D and upgrades.

- Sales & marketing: Subsidies, promotional events, and operating costs for major shopping festivals.

- Logistics & fulfillment: Warehouse and delivery network costs, including some merchant and customer delivery subsidies borne by the e-commerce segment.

- Merchant support & content moderation: Customer service, risk control, ecosystem maintenance and other operational expenditures.

2. Cloud Intelligence Business

Revenue Drivers:

- Core cloud services (IaaS/PaaS): Pay-as-you-go and subscription-based offerings for computing, storage, databases, and other foundational services.

- AI and value-added products: High value-add services such as GPU computing, AI model hosting, and big data analytics.

- Enterprise customized solutions: Hybrid cloud, private cloud, and industry-specific solutions.

- DingTalk SaaS integration: Cloud resource usage and subscription revenue driven by workplace collaboration via the DingTalk platform.

Cost Drivers:

- Data center construction & depreciation: Capex on hardware, power, cooling, etc., leading to depreciation costs.

- R&D investment: Continued funding for AI technology development and cloud product innovation.

- Customer acquisition & support: Marketing spend and pre-sales/post-sales support teams.

- Scaling operations & efficiency: As revenue grows, unit costs can decline, but the business is still in an expansionary investment phase.

3. Digital Media & Entertainment

Revenue Drivers:

- Video advertising (Youku): Relies primarily on user traffic and increased advertising spend.

- Paid memberships: VIP subscriptions provide a secondary revenue stream, with untapped potential.

- Content production & distribution: Box office, licensing, and derivative revenue from films and TV series.

Cost Drivers:

- Content acquisition & original production: Licensing fees and production costs constitute the largest expenses.

- Bandwidth & technology: CDN and server costs driven by high video streaming traffic.

- Marketing & user acquisition: User outreach, promotional campaigns, and subscription incentives.

- Production teams & talent: Expenditures for actors, directors, and platform staff.

4. Innovation Initiatives & Others

Revenue Drivers:

- DingTalk (paid subscriptions & value-add): A massive user base where premium features drive revenue.

- Gaode Map (advertising & commissions): Location-based services, ride-hailing, and local commerce referrals generating ad and commission income.

- Other emerging businesses: Smart hardware, travel platforms, etc., which are still in early incubation stages.

Cost Drivers:

- R&D: Significant investment in technological iteration and product innovation.

- User subsidies & market expansion: Costs from free user offerings and early-stage market promotion.

- Infrastructure & operations: Additional spend on data updates and security on top of leveraging cloud resources.

- Strategic investments & integration: Exploration of frontier fields like autonomous driving and ecosystem plug-ins.

Cross-segment Synergy & Ecosystem Advantages

- E-commerce & Cloud: E-commerce's high-concurrency scenarios validate cloud capabilities, while cloud services provide AI and data support to e-commerce.

- E-commerce & Media: Bundling advertising and memberships creates a virtuous cycle of user retention and conversion to spending.

- Cloud & DingTalk: Workplace collaboration (via DingTalk) helps cloud services penetrate enterprise markets.

- Gaode & Local Services: Traffic from mapping and transportation feeds into e-commerce and O2O service deployments.

Through the mutual support of traffic and technology across its businesses, Alibaba has built a powerful synergy in its revenue and user ecosystem: e-commerce continuously generates cash flow, cloud computing reinforces the technological moat, and media & innovation units enhance user stickiness and future growth potential.

4. Performance & Trend Analysis

Operating Trends

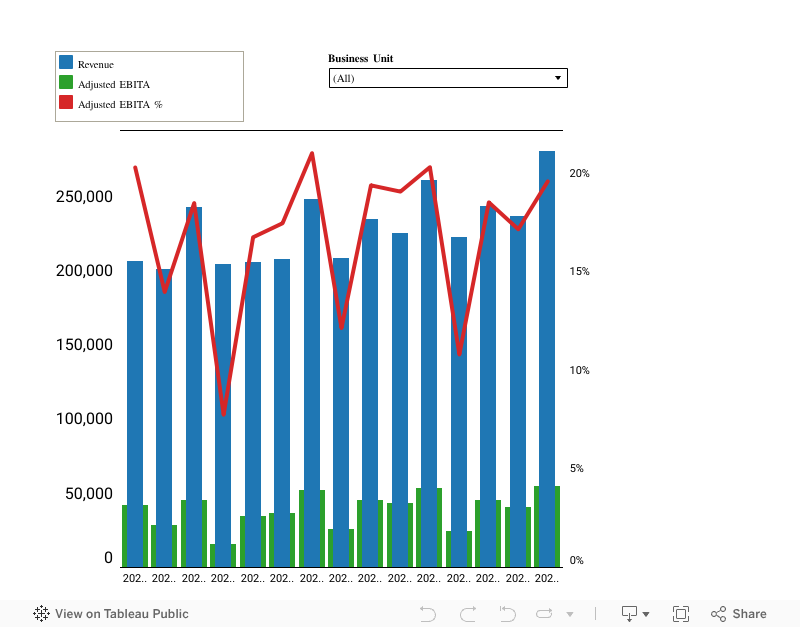

After a phase of challenges, Alibaba has returned to a modest growth trajectory. On the revenue side, thanks to the recovery of core e-commerce and AI-driven expansion in the cloud business. FY2025 Q3 revenue increased 7.6% YoY to RMB 280.15 bn, accelerating from 5.2% in the previous quarter and showing a clear rebound. On profitability, cost optimization and operating leverage have improved efficiency, with FY2025 Q3 consolidated adjusted EBITA up 3.8% YoY to RMB 54.85 bn.

China Commerce (Taobao and Tmall Group)

FY2025 Q3 revenue grew 5.4% YoY to RMB 136.09 bn. Customer management revenue (CMR) increased by 9.4% to RMB 100.09 bn, mainly driven by an improved take rate and GMV growth. In particular, the introduction of a new 0.6% technology service fee on merchants last September and revenue contributions from the new marketing tool Quanzhantui both helped lift the platform's take rate. As Alibaba's largest profit source, TTG's adjusted EBITA for the quarter grew to RMB 61.08 bn, turning positive with 1.9% YoY growth. Given management's focus on stabilizing market share as a mid-to-long-term goal, TTG's profitability is expected to remain volatile in the short term.

International Commerce (AIDC)

In FY2025 Q3, AIDC revenue was RMB 37.76 bn, up 32.4% YoY, continuing to be the fastest-growing segment within the group. Core drivers were revenue growth in cross-border retail (AliExpress and Trendyol, up 36% YoY) and robust expansion of the wholesale business. Adjusted EBITA loss in the period widened by 57.4% YoY to RMB 4.95 bn. The primary drags were marketing subsidies during overseas shopping festivals and continued customer acquisition investments in Europe and the Gulf region.

Cloud Intelligence (Alibaba Cloud)

Alibaba Cloud's FY2025 Q3 revenue grew 13.1% YoY to RMB 31.74 bn, returning to double-digit growth and indicating that the previous slowdown has been reversed. Growth was fueled mainly by strong demand for public cloud services, especially a surge in demand for AI-related cloud products. Alibaba Cloud's AI-related product revenue has maintained triple-digit YoY growth for six consecutive quarters, becoming the core driver of the cloud segment's growth. Management expects the cloud business will benefit from continued AI application rollouts, further boosting its growth rate. On the profitability side, cloud adjusted EBITA reached RMB 3.14 bn, up 32.7% YoY. This sharp profit increase was driven by business structure optimization and improved operational efficiency, cloud revenue mix is tilting toward higher-margin public cloud products. Overall, Alibaba Cloud's growth momentum has strengthened significantly, reversing the prior deceleration trend.

Alibaba Cloud announced a plan to invest over RMB 380 bn in cloud computing and AI infrastructure over the next three years — an amount exceeding its total investments in the past decade. According to Goldman Sachs estimates, roughly 80% of this plan will go toward building AI server clusters, with the remaining funds for general servers and data center support. Based on current pricing for state-of-the-art AI servers (training/inference) and projected utilization, combined with high single-digit growth in public cloud revenue, Alibaba Cloud's revenue could achieve 20%+ growth over the next two years. Notably, as capex increases, depreciation and amortization (on a 3–5 year cycle) will also rise markedly, potentially pressuring cloud margins in the short term. Looking at the trajectories of global top cloud providers (AWS/Azure/GCP), periods of peak infrastructure investment often accompany: 1) continued expansion in revenue scale; 2) a lag before scale efficiencies kick in. Given that AI cloud services carry significantly higher EBITA margins than the public cloud average, we believe that although Alibaba Cloud's margins will face depreciation pressure, with technological optimizations and a rising share of AI-driven revenue, adjusted EBITA margins should remain on a steady upward trend.

Other Segments

Cainiao (Logistics): Revenue was RMB 28.24 bn, a slight 0.8% YoY decline mainly due to an internal reallocation of Alibaba's e-commerce logistics business (certain logistics revenue was shifted to the e-commerce segment). Adjusted EBITA came in at RMB 0.24 bn, down 75.5% YoY, primarily dragged by narrower margins in cross-border fulfillment solutions and reduced profitability in domestic logistics services. Local Services: Revenue grew 12% YoY to RMB 16.99 bn, as order volume growth drove increases in food delivery and mobility services, along with higher local advertising income. Benefiting from improved operational efficiency and economies of scale, adjusted EBITA loss narrowed by 71.2% YoY to RMB 0.6 bn, edging closer to the breakeven point. Digital Media & Entertainment: Revenue rose 7.9% YoY to RMB 5.44 bn, mainly thanks to a rebound in Youku's advertising revenue. Adjusted EBITA loss narrowed by 40.2% to RMB 0.31 bn.

5. Valuation Analysis

Valuation Methodology and Key Assumptions

Methodology: Sum-of-the-Parts (SOTP).

Multiple selection: Based on each segment's growth profile, profitability, and comparable company trading ranges (see table below).

Base Case SOTP Summary (FY2025E)

China Commerce (TTG) Valuation

As Alibaba's primary cash cow, TTG boasts stable profitability and cash flow, but with China's e-commerce penetration nearing saturation, its long-term growth rate is relatively moderate. We assign a 9× EV/EBITA multiple. For reference, domestic peer Pinduoduo is currently around 20× P/E, corresponding to roughly 10–15× EV/EBITDA. Therefore, 9× EV/EBITA for TTG is a reasonable yet somewhat cautious valuation.

International Commerce (AIDC) Valuation

AIDC is still in an expansionary phase and overall unprofitable, so we apply a 1.5× EV/Revenue multiple. This is informed by global emerging-market e-commerce valuations: for instance, Sea Ltd's e-commerce business and MercadoLibre trade around 1–2× P/S. Considering that AliExpress, Lazada, etc., have significant growth potential in emerging markets but are not yet profitable, we take the midpoint at 1.5×.

Cloud Intelligence (Alibaba Cloud) Valuation

As the key growth engine for Alibaba, we use a 3× EV/Revenue multiple for the cloud segment. Noting that global cloud leaders AWS and Azure command higher implied valuations (~5–7× revenue) with mature profitability, we take a suitably conservative stance for Alibaba Cloud by applying a discount to the global leaders' multiples, reflecting that its profit margins are still in an improvement phase and regulatory conditions add uncertainty.

Local Services Valuation

The local services segment has significantly narrowed its losses and possesses considerable user base and order volume growth potential. We assign a 2× EV/Revenue multiple to this segment. By comparison, Meituan currently trades at about 2–3× P/S, but Meituan is profitable and growing faster, whereas Ele.me and others are still catching up. Thus, 2× revenue is a reasonably cautious valuation for Alibaba's local services, with upside for a higher multiple if and when it achieves breakeven.

Cainiao Logistics Valuation

For the Cainiao logistics business, we apply a 0.7× EV/Revenue multiple. In recent years Cainiao has delivered steady growth but with low margins, so we opt for a lower revenue multiple to reflect this. As a reference, JD Logistics was around 0.4× P/S at the end of 2024, whereas Cainiao's market fundraising valuation in 2023 reached roughly RMB 150 bn (about 1.4× revenue). We choose a value between these, indicating that Cainiao's asset-light, technology-driven model (with advantages in cross-border and warehouse networks) warrants a slightly higher multiple than traditional logistics companies, yet given macro volatility and profit pressures, below its peak valuation.

Digital Media & Entertainment Valuation

The digital media segment is currently small in scale and not very profitable. Referencing iQiyi's current ~0.8× EV/Revenue multiple, we assign it a similar 0.8× multiple.

Non-operating Items Adjustments

- Net Cash: According to the FY2025 Q3 financials, Alibaba had cash and cash equivalents of RMB 162.78 bn and short-term investments of RMB 236.95 bn. In our base scenario, treating RMB 210.31 bn of treasury investments as cash per management's approach, and with total interest-bearing debt of RMB 231.53 bn, net cash amounts to RMB 378.51 bn.

- Ant Group: We reference Ant Group's valuation based on an internal share buyback in July 2023 at RMB 567.1 bn, which implies a value of RMB 187.14 bn for Alibaba's 33% equity stake. Due to regulatory uncertainty and limited liquidity, we apply a 30% discount to Ant's overall valuation, resulting in an adjusted value of RMB 131.0 bn.

6. Risk Analysis

Alibaba faces several key risks despite its diversified business portfolio and core competitive strengths:

Geopolitical Frictions Escalation (High Risk): Heightened U.S.-China tech export controls and trade barriers could directly impact Alibaba's cross-border e-commerce business, or pressure the growth and margins of its international operations. Geopolitical uncertainty may also shrink market risk appetite, weighing on valuation. Although the company is accelerating expansion in emerging markets like Southeast Asia (Lazada) and the Middle East (Trendyol), the short-term offset to these risks is limited.

China Regulatory & Policy Risk (Medium-High Risk): In recent years, the Chinese government has tightened oversight of the internet and tech industry, including antitrust measures, data security, and algorithm scrutiny. Although regulatory pressure on Alibaba has somewhat eased (with Ant Group's fine settled and supportive signals for the platform economy), the policy environment remains uncertain. Alibaba must continue to invest in compliance and seek growth within regulatory bounds, which could increase costs or limit expansion of certain businesses.

Intensifying Industry Competition (Medium Risk): Alibaba faces increasingly fierce competition across its sectors. In e-commerce, Pinduoduo targets lower-tier markets and value-for-money, Douyin (TikTok) e-commerce is rapidly rising via content-driven traffic, and JD.com continues to fortify its supply chain edge – all posing multi-front pressure on Alibaba's user traffic and market share. In cloud computing, Tencent Cloud, Huawei Cloud, and global players like AWS and Azure are competing in China, squeezing Alibaba Cloud's market share. In local services, competition with Meituan remains intense. This multifaceted competition will raise customer acquisition costs and potentially squeeze overall profit margins.

Macro Economy & Consumer Trend (Medium Risk): Alibaba's performance is closely tied to macroeconomic and consumer trends. If China's economic recovery falls short of expectations or consumer confidence remains weak, it would dampen GMV growth in Alibaba's core commerce business and weigh on advertising and commission revenues. If the global economy slips into recession, it would similarly constrain cross-border trade volumes and corporate cloud IT spending.

Strategic Execution & Investment Return Risk (Medium Risk): There is uncertainty whether Alibaba's RMB 380 bn capex plan over the next three years will generate the expected returns. If AI commercialization progresses more slowly than anticipated, or if the payoff period for cloud infrastructure investments lengthens, it could create a short-term drag on the company's earnings.

These risk factors, individually or in combination, could adversely impact Alibaba's growth outlook and valuation.

Disclaimer

This report reflects only the author's personal research and analysis of the company and is provided for informational purposes. It does not constitute any stock recommendation or investment advice. Readers should make independent judgments and assume responsibility for their own investment decisions; the author is not liable for any consequences arising from the use of this report.

The views expressed in this report are the author's personal opinions and do not represent the positions of the author's employer or any other institution.

All information and data cited in this report come from publicly available sources. The author has endeavored to ensure accuracy and reliability, but makes no explicit or implied warranty as to the accuracy or completeness of the information cited.